Risk Exposure Score

- How Protected Is Your Capital in a Global Crisis?

If your country becomes unstable - what’s your plan B?

Calculate your Risk Exposure Score:

In just 90 seconds, discover how exposed your wealth is to geopolitical shocks, financial instability, and global disruptions.

/Built using the same principles applied by ultra-high-net-worth investors./

Private. Confidential. Designed for serious investors only.

Most Investors Are Not Prepared for What’s Coming.

The world is becoming increasingly unstable.

- Geopolitical tensions are rising.

- Financial systems are fragmenting.

- Capital controls are quietly expanding.

Yet most investors still operate with:

capital concentrated in one country

limited liquidity

no relocation strategy

no global backup plan

The real risk is not market volatility.

👉 The real risk is being unprepared when access disappears.

What Smart Capital Is Doing Differently?

Ultra-high-net-worth investors don’t rely on predictions.

They build resilient structures.

They ensure:

multi-jurisdictional asset allocation

global banking access

liquidity under stress

mobility across borders

This is exactly what the Risk Exposure Score is designed to evaluate.

Find Out Where You Stand — Before It Matters.

Your capital deserves more than assumptions.

What Is the Risk Exposure Score?

A proprietary assessment that analyzes your exposure across four critical dimensions:

🌍 Geo Risk

Where your capital is exposed globally

🏢 Asset Structure

How your wealth is distributed

💧 Liquidity

How fast you can access your money

✈️ Mobility

How quickly you can act if needed

In under a minute, you’ll understand where you stand — and what needs to change. What You’ll Discover:

- Your personal Risk Exposure Score (0–100)

Your vulnerability level in a crisis scenario

The weakest points in your current structure

Strategic recommendations to strengthen your position

👉 Most investors have never seen their risk this clearly.

How It Works

- Answer 12 quick questions

Get your Risk Exposure Score

Receive tailored insights

(Optional) Unlock your personalized strategy

⏱ Takes less than 90 seconds

How Protected Is Your

Capital in a Crisis?

Answer 12 questions in under 90 seconds. Receive your personalised Risk Exposure Score — an institutional-grade assessment of how vulnerable your wealth is to geopolitical, financial, and structural shocks.

A specialist from Virt Realty will be in touch shortly.

If your score reveals exposure, the next step is clarity.

/Used in private investor advisory/

We work with a select number of investors to:

restructure global portfolios

secure capital across jurisdictions

design crisis-resilient strategies

👉 Request a Private Strategy Session

Confidential & discreet

Designed for high-value investors

No public data sharing

How the Ultra-Wealthy Actually Hedge Their Risks and prepare for Black Swan events:

1) Geographic Diversification (the most basic, yet critical)

They never keep everything in a single jurisdiction—even if it’s the United Arab Emirates.

Typical structure:

- Middle East (liquidity, transactions, growth) — Dubai

- Europe — Switzerland / United Kingdom

- Asia — Singapore

- sometimes the U.S. — United States

📌 The point:

if a region is “temporarily unstable” → capital and life continue elsewhere.

2) “Second residency / passport strategy”

Almost everyone has:

- 2–4 residencies

- 1–2 alternative citizenships

Why this is important:

👉 In the event of a crisis, borders close

👉 But not for residents/citizens

This provides:

- quick exit

- access to the banking system

- legal status in another country

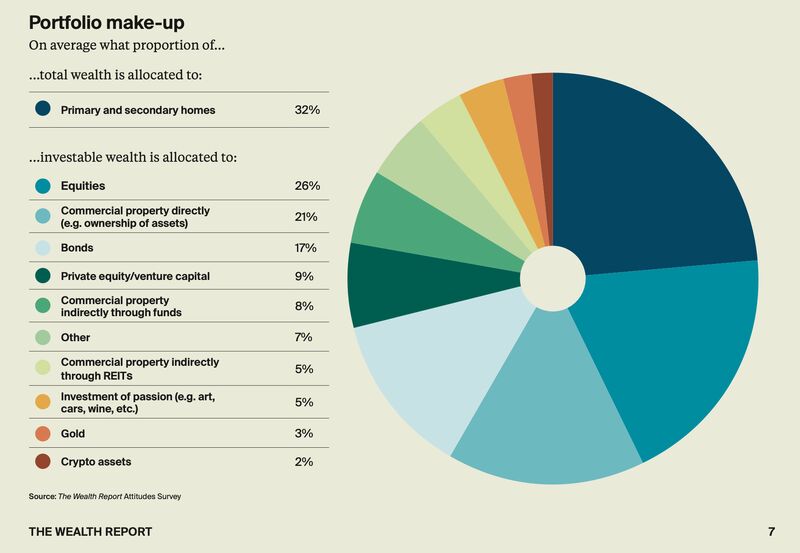

3) Asset allocation by type

They don’t keep everything in real estate.

The structure is usually as follows:

- 30–50% — real estate (often in Dubai)

- 20–40% — liquid assets (stocks, funds)

- 10–20% — private equity / deals

- 5–15% — “safety net assets”

“Safety net assets”:

- gold

- dollar-denominated instruments

- sometimes crypto

📌 Logic:

if a shock occurs → liquid assets provide flexibility.

4) Banking diversification

Not just one bank. Not even just one country.

Typically:

- a bank in the United Arab Emirates

- a bank in Switzerland

- a bank in Singapore

👉 if there are restrictions somewhere → money is accessible elsewhere.

5) Insurance (but not as people think)

Important:

- Traditional insurance provides almost no coverage for nuclear risks

BUT the following are used:

- political risk insurance (for businesses)

- asset protection structures (trusts, funds)

- relocation/evacuation insurance (a very niche product)

6) Evacuation plan (yes, almost all UHNW individuals have one)

This isn’t “panic”; it’s a protocol.

Typically includes:

- pre-selected destinations (e.g.,- Switzerland / Singapore)

- access to private aviation

- prepared documents

- immediate liquidity